|

| |

Companies/Brokers/MGAs

Do you have a new product or enhancement?

Click here to submit your information

—OR—

call 1-800-428-4384 to speak to

Eric Hall Executive Vice President - Advertising, National Sales Director |

|

| |

| INSURANCE MARKETPLACE SOLUTIONS |

|

| |

|

|

Accountants

Could a single accounting rule change have caused our current financial crisis? The Financial Accounting Standards Board (FASB) implemented FAS 157 on November 15, 2007. This new rule guides accountants in setting the fair market value of a financial asset. Prior to its implementation, a financial instrument was valued at its purchase price. Following implementation, the value of these instruments is based on the market value as of the end of the trading day.

According to some, this rule caused the cascading financial crisis. As financial stocks started to tumble, companies were forced to restate their net worth every day. Some financial assets became so toxic that there was no market for them at all. This caused the net worth of a number of financial companies to tumble. And, as their net worth tumbled, their ability to loan or borrow money also tumbled.

Whether the theory is accurate or not, it is important to remember that accountants do not make the rules. They simply follow them. The public expects the accounting profession to apply a consistent, professional approach to the preparation of financial statements that fully complies with all FASB standards

|

| |

|

|

| |

| The Accountants Marketplace |

| |

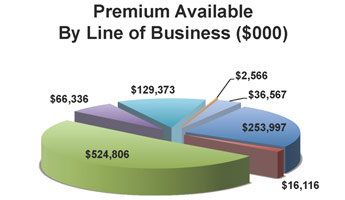

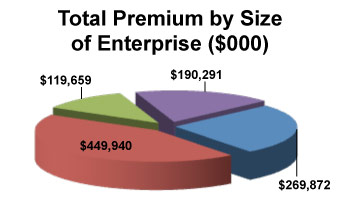

There are over 480,000 accounting type businesses in the United States. The premium generated by them is over $1 billion. Firms that have no employees combined with those employing fewer than 50 employees pay 70% of that premium. Accounting firms buy all types of insurance but more than half of their premium dollar goes for their liability coverage.

For more information:

MarketStance website: www.marketstance.com

Email: info@marketstance.com |

| |

|

| |

|

We are in the midst of a confidence crisis. It centers on our financial institutions and spreads out from there. At the heart of everything is the accounting community. It provides the financial statements necessary for businesses to understand their current status and to provide projections for the coming year.

Important end of the year tax-related decisions are being made at this time. Many of the actions currently being taken are based on tax advice from accountants. Should bonuses be given or deferred? Which stocks should be retained and which sold? How should the total financial portfolio be adjusted to provide the highest rate of return and the lowest taxes? Accountants provide predictive models based on the current rules so that businesses can make rational decisions. Accountants are expected to present the hard facts. It is up to the business to make decisions based on those facts.

|

| |

|

| |

|

Here is a possible claim scenario:

Margola Enterprises was considering purchasing Binginham Brothers. It requested a complete set of financial statements. After analyzing the statements, it purchased Binginham. Margola was shocked when it actually took over the business, completed a physical inventory and discovered that the value of the stock was significantly less than the value that appeared in the statements. Rather than accusing Binginham Brothers of lying, Margola believed that By the Book, Inc., Binginham Brothers’ accounting firm, valued the inventory on a "Last In First Out" (LIFO) basis instead of on the standard "First in First Out" (FIFO) method.

Margola sued By the Book, Inc., arguing that it used a “non traditional valuation system” for the stock and did not provide a disclosure statement. As a result, Margola paid more than the true value of the company. |

| |

|

| |

|

Accountants professional liability coverage is readily available and much needed, according to our experts. Chris Zoidis, vice president and director, SRD-International at Burns & Wilcox states, “All accountants should buy this coverage to protect themselves against errors and omissions in performing accounting services.”

Accountants professional is not just for Certified Public Accountants (CPA's). Michelle A. Duffett, executive vice president, Insight Insurance Services, Inc., points out that, “Even a small firm, or a bookkeeping or tax only practice, is not immune from the possibility of a professional liability claim. You don't have to make a professional error to be sued. You only need an unhappy client that believes you did not arrive at the desired result.”

The American Institute of Certified Public Accountants (AICPA) endorses a program from CNA. This program, according to Jeff Day, assistant vice president at CNA, has three tiers uniquely tailored to the different needs of small, medium and large firms. AON is the MGU for this program.

John Torvi, director of marketing and sales at The Herbert H. Landy Insurance Agency, advises that his firm is an MGA for a program designed for accounting firms of all sizes that has no CPA requirement. He states, “The coverage is designed for individuals or firms in practice areas from bookkeeping and tax preparation to business valuation, financial planning and investments services, audits, software, technology consulting and more.”

Click here for the complete article …

|

| |

|

| |

MANAGING GENERAL AGENTS

INSURANCE COMPANIES |

| |

| |

|

|

|

|

|

|

| |

| |

This message was sent by The Rough Notes Company, Inc.,

11690 Technology Drive, Carmel, Indiana, 46032

1-800-428-4384

|