|

Here is a possible loss scenario:

Sounds Like a Great Idea Academy specializes in entrepreneurial training. Its goal is to encourage fifth-graders through high school seniors to develop innovative ideas that can translate into business opportunities that can support them when they graduate from high school. John and Joan are sixth graders who partnered on a great idea that they want to explore. Their instructor, Ms. Fleming, and the principal, Mr. Prescott, have reviewed the project and agree with the prospectus.

John and Joan decide to test their product and provide free samples to a number of their classmates.

Some of them become ill, and once the parents discover the connection between the free samples and the illnesses, a lawsuit is filed against Sounds Like a Great Idea Academy, Ms. Fleming, and Mr. Prescott. |

|

|

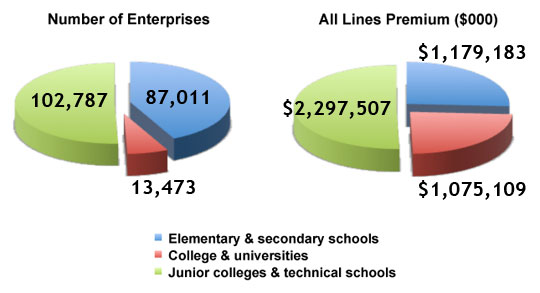

The marketplace for educational institutions is quite varied. Some insurance companies and brokers that provide the coverage have very broad appetites while others are more limited.

“We specialize in private, K-12, community colleges, small- to mid-size four-year colleges, small- to mid-size universities, and various types of vocational/technical schools,” explains Shirl Hedges, underwriting manager at Philadelphia Insurance.

Tony Armor, commercial underwriter/business development at Roush Insurance Services, Inc., says, ”We can place coverage for all types of educational institutions. However, we most often receive submissions for vocational/technical schools such as construction, welding, and apprentice training.” He states that these types of risks are usually written on nonadmitted paper.

WRM America is in the market for most types of schools. Its president, Steven E. Sims, says, “WRM America provides a comprehensive program of coverages to public and private K-12 schools, public and private colleges and universities, and vocational/technical schools.”

Connie R. Reynolds, vice president, school programs at Glatfelter Public Practice, explains that it has a slightly different approach. “We write private and public K-12, junior colleges, and community colleges, but we don’t write universities. We write vocational/technical schools, but not driver training schools or certain others. We can also write nursing school programs and other two-year programs.”

School exposures include property, liability, automobile, EPLI, and workers compensation. According to Ms. Hedges, two unique and important exposures are failure to educate and violent events.

Mr. Sims points to the broad nature of the exposure. “Complicating traditional risks is the fact that schools are often used by outside parties and members of the general public for activities such as religious services, recreational sports leagues, elections, and other community events."

“From a liability standpoint, the most common exposure is sexual/physical abuse and injury to students or athletes," according to Mr. Armor. "With schools placing a great deal of emphasis on athletics and academics, many students spend almost as much time at school with training, practices, tutoring and/or research as they do at home. As a result, there is greater potential for both bodily and personal injury for athletes and other students who may find themselves in situations that could compromise their safety.”

Click here for the complete article … |

|