The Rough Notes Company's FSAC division will be headed by Gary Lesser (left) and Bill Clemmer who developed the Plan Illustration Software CD to help agents create professional presentations.

Starting next month The Rough Notes Company will take a more active role in helping agents and brokers serve the financial services needs of their commercial clients. Financial Services Agency Consulting (FSAC) is a newly-created division of The Rough Notes Company which will support agents in selling financial services--particularly retirement planning products.

FSAC is headed by Bill Clemmer and Gary Lesser, two career financial service professionals who will assist agents in plan analysis, design, and placement. FSAC's services will take a variety of forms--including phone consultations, retirement planning software, seminar speaking and personal presentations--depending on an agent's needs.

Gary S. Lesser, JD, is a nationally known consultant, author, educator and speaker on retirement plans. William A. (Bill) Clemmer has more than 25 years of experience in the financial services industry on Wall Street. His areas of expertise include marketing of financial services and products, consultative sales of 401(k) programs, field force management and team building, training and motivation.

Developing the tools

In order to provide property/casualty agents with updated information on financial services on a continuing basis, Lesser and Clemmer will be co-authoring a monthly financial services column in Rough Notes magazine called "It's All About Money," starting in the September issue.

The first article will be an overview of FSAC's services as well as an introduction of the principals. It will be followed by comprehensive articles on financial services marketing and will discuss tools such as pension plans, IRA's 13 faces, the Roth IRA, Keoghs and retirement benefits. Eventually, the column will consider just about every subject a producer should be familiar with in order to be successful in closing retirement plan sales, especially to existent property/casualty clients.

Agents are invited to call (toll-free) (800) 428-4384 to request their free, no-obligation Retirement Plan Marketing Kit. Also to be made available almost immediately, is a comprehensive, interactive retirement plan software CD. This nominally priced product is a sales tool for agents who are prepared to offer their better property/casualty clients an opportunity to review existing benefits programs and to explore appropriate retirement plans, products and related services.

"This Kit, which is available to agents and brokers merely for the asking," says Gary Lesser, "provides all of the information he or she needs in order to embark upon a sales effort which will prove to be remarkably rewarding. And because The Rough Notes Company has decided to subsidize this important service, the entire cost to agents and brokers is extraordinarily modest," Lesser adds--"much less, for example, than they might consider reasonable when ceding certain commissions to wholesalers or program administrators for P-C coverage placement."

Bill Clemmer further explains that this new Rough Notes service is not designed only to provide information for agents. "We're serious marketers," Bill says, "and we're prepared not only to answer questions and offer advice--we're even ready to go out in the field and accompany an agent or broker on serious, complicated sales calls. Effectively," he continues, "when we are invited, we are going to function as an arm of the agency or brokerage and, to the extent it is requested, we are prepared to take a hands-on approach in order to help our property/casualty friends compete seriously for this important business."

If, as often has been stated, an independent agent's best prospects for new coverages are indeed his/her own best customers, property and casualty agents and brokers have a built-in, viable prospect list for the sale of a number of new coverages, with special emphasis on the very lucrative benefits market. (See box on page 47.)

In conducting in-depth research for a marketing book for independent property/casualty agents, this author learned that as skeptical as people might be about insurance companies and how they operate, they trust the agent or broker they know and deal with and want to continue to confide in him/her when it comes to serious insurance expenditures and buying the right coverages at the most competitive rates. That information, alone, suggests that P/C producers should have a distinct advantage in developing their prospect list.

Bill Clemmer has more than 25 years experience in the financial services industry on Wall Street.

Bill Clemmer has more than 25 years experience in the financial services industry on Wall Street.

Who are the best prospects for retirement plans?

There's a (happy) surprise answer to that question, according to Bill and Gary. And the answer is that virtually all of the larger commercial clients in an agency's x files are legitimate candidates for retirement plan solicitation. Here's why. According to Gary Lesser, "Your client either has, or doesn't have, a 401(k) or similar profit sharing plan for him or herself and his/her employees. If they do not have a plan in force, obviously they are going to need one very quickly to remain competitive in this hard-to-come-by-good-employees market. If they do have a plan and probably many, if not most, will, don't discount them as prospects," says Gary, emphatically. "About 25% of all 401(k) plans have a change of administrator in a given year. That means over a period of just four years, there is a likelihood that every single client with a program in position, will be seriously prepared to listen to a reasonable alternative--especially from someone they do business with, and trust."

"There are four areas that lead to unhappiness with the relationship," Bill Clemmer explains. "The most important one has to do with administration--the simple paperwork. Is it being done? Is it being done right? Is it being done consistently? The second possible failing is simply responsiveness to questions. Does the 401(k) administrator call you back promptly with answers?

Gary Lesser is a nationally known consultant, author, educator and speaker on retirement plans.

Gary Lesser is a nationally known consultant, author, educator and speaker on retirement plans.

"Third," he points out, "there is the overall servicing factor, including record keeping, which leads (of course) to the cost of the plan. Finally," he says, "there is sometimes discontent with the investments. Bottom line, agents who receive the right kind of support can get a hearing for an alternative proposal nearly 100% of the time. And we are ready, able and willing to provide that right kind of support." (See box on page 47.)

Gary Lesser suggests that the first step, as in most selling operations, is to prepare a viable prospect list and to do so with confidence. He continues, "In addition to preparing P-C agents for the initial interview, we're going to stay with them and provide whatever additional help is needed. They can count on very friendly hand-holding from us and, when the time comes, they will be introduced to professionals we know and have worked with and who they can truly rely upon. And we're here for the long pull. Just as The Rough Notes Company has been serving agent needs for well over 100 years, we see this service of ours, in partnership with Rough Notes, continuing throughout the 21st century."

Another weapon in the Financial Services Agency Consulting arsenal are seminars which Clemmer and Lesser base upon the comprehensive information they have been delivering for many years to all types of audiences. The first seminar is tooled specifically for property/casualty agents and will be presented in several locations around the country. Announcements will be made for specific times and places.

The second seminar is actually designed to be a selling tool for the

P-C agent and broker--directed to actual prospects. Agents will be able to invite Gary and Bill in for a breakfast or lunch meeting--or even a straight presentation--with a group of their clients or their clients' tax/legal advisors. In Bill and Gary's experience, the most effective group consists of about 30 participants, but should not exceed 50, so that there is plenty of time to answer everyone's questions.

By utilizing this sales approach, agents are demonstrating not only their knowledge but their ability to provide an important service to their clients, and the willingness of these experts to go the extra mile for their business. According to Clemmer and Lesser, agents are going to be very pleasantly surprised at how many sales can be closed by utilizing this method.

Gary Lesser summarizes the business plan. "Simply stated," he says, "we know there is an enormous amount of business that P-C agents can pick up with remarkably little effort, and we are determined to provide them with every advantage in order to do so. This is a no-fail concept in my view." He continues, "As I see it, there are literally thousands of dollars in commissions being left on the table which will be collected by someone else if P-C agents don't approach these prospects. And, best of all, since there is almost certainly some discontent on the part of most business owners, agents are actually solidifying their relationships in a sense by 'coming to the rescue.'"

He concludes his summary by pointing out what has been documented in study after study of insurance buying habits of individuals and commercial clients. "When agents sell financial services and/or benefits to their property/casualty clients, their persistency rate is dramatically increased. So it stands to reason that agents are in a win-win situation in soliciting this new business. Not only do they increase revenue, they solidify the account and protect their existent P-C business from being 'pirated' by an aggressive Life/A&H sales person who is also looking to expand his or her horizons." *

Let's assume that you decide to take advantage of the seminar we discussed earlier which, effectively, would be a continuing education program for accountants in your selling area. Let's also assume that one of those accountants requested a retirement plan proposal he heard mentioned at the seminar for his own business.

This accountant might very well have 35 full-time employees, and their annual payroll might well be about $1 million. Let's further assume that he has an existing profit sharing plan with 401(k) features and assets of $3 million. You have discovered that he is somewhat unhappy with the services the plan receives from its service providers.

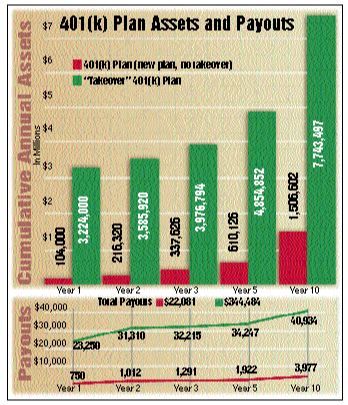

With the above information, you complete a one-page proposal request form and forward it to Financial Services Agency Consulting (FSAC). The turn-key 401(k) proposal is ultimately accepted and it provides for a matching contribution of 25% of a participant's contribution up to 5% of salary. If employees defer the national average of 4% ($40,000) and the employer makes a 5% profit sharing contribution ($50,000), the plan will receive $100,000 (including the matching contribution of $10,000) in new assets each year.

The prospects look good that both you and the client will be happy. The investment package selected by the client will provide a series of annual payments to the agent equal to (a) 3/4 of 1% on all new contributions, plus (b) 1/2% of assets under management after 12 months and held on the last day of the year. A summary of plan assets and payouts for years 1,2,3,5 and 10 are shown in the above chart.

Finally, because your accountant client was so pleased with his new plan and investment program, he now is recommending you to his clients. It's pretty easy to see how recurring annual contributions, irrespective of market conditions, could dramatically affect your bottom line.

When fully implemented, Financial Services Agency Consulting (FSAC) will provide assistance in the following areas:

* Educational seminars for accountants, planners, brokers and agents

* Telephone consulting and client conference calling

* Retirement Plan Services

--Plan adoption services

--SEP, SARSEP, SIMPLE plan illustrations

--Turn-key 401(k) plan with administration and enrollment services. Fully automated at every level

--Pension and profit-sharing plan availability

--457 and 403(b) plan support

--Minimum required distribution (MRD) and substantially equal periodic payment calculations

--Software support and telephone tutorials

* Financial Services

--Mutual funds

--Variable annuities

--Product and marketing support

--A wide variety of financial and tax calculations

©COPYRIGHT: The Rough Notes Magazine, 1999