Keogh--then SEP and SIMPLE. And now, the "Mini-K" for the very small, one-person business! The promise of a significantly enhanced 401(k) is now possible to these businesses based on a combination of features contained in the new tax law.

Keogh--then SEP and SIMPLE. And now, the "Mini-K" for the very small, one-person business! The promise of a significantly enhanced 401(k) is now possible to these businesses based on a combination of features contained in the new tax law.

IT'S ALL ABOUT MONEY

New tax laws benefit the smallest of businesses

By William A. Clemmer & Gary S. Lesser, Esq.

Keogh--then SEP and SIMPLE. And now, the "Mini-K" for the very small, one-person business! The promise of a significantly enhanced 401(k) is now possible to these businesses based on a combination of features contained in the new tax law.

As part of a renewed focus to increase retirement savings, the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) raised the limits on annual contributions to tax-favored plans, including Keoghs and SIMPLE Plans. On scrutiny, we find that there is a little-noticed (thus far) advantage for the small business owner. It is this: By combining several of the law's new provisions, a sole owner business can contribute and thus accumulate unusually large sums in 401(k) plans beginning next year (2002).

Until now, contributions have been limited to 15% of compensation. This plus plan costs (set-up and maintenance fees) made 401(k) plans out of reach for most small businesses.

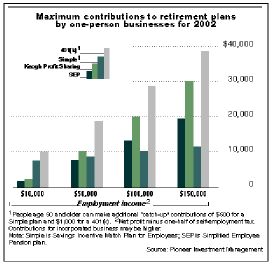

However, the new law offers a combination of business and individual contributions, which raises this contribution level to over 28% (depending upon the individual's compensation). Thus, an individual earning $100,000 in a one-person unincorporated business will be able to contribute approximately $28,000 into a 401(k) in 2002; $40,000 at the new $200,000 compensation cap. This is thousands of dollars more than can be contributed to other types of tax-deferred plans! In addition, several mutual fund companies are rolling out a "mini-K" with much lower plan costs. Voilà, 401(k) for the little guy!

401(k) plans, which allow employees to contribute a portion of their salaries on a pre-tax (tax advantaged) basis, are the norm in larger corporations. Lower costs due to packaged plans and maintenance plus mutual funds and annuities have made these plans available to smaller corporations. However, they are seldom found in the smallest businesses. A one-man 401(k) simply did not make sense under current law (pre-EGTRRA). Other plans are less complicated, cheaper to set up and maintain, and often allow larger contributions.

401(k) plans, which allow employees to contribute a portion of their salaries on a pre-tax (tax advantaged) basis, are the norm in larger corporations. Lower costs due to packaged plans and maintenance plus mutual funds and annuities have made these plans available to smaller corporations. However, they are seldom found in the smallest businesses. A one-man 401(k) simply did not make sense under current law (pre-EGTRRA). Other plans are less complicated, cheaper to set up and maintain, and often allow larger contributions.

One of the first to offer and promote the new possibilities is Pioneer Investment Management in Boston. The new law "changes the rules in a way that allows one-person businesses to do truly amazing things with 401(k) plans," says Marcy Supovtiz, a senior managing director at Pioneer.

Financial advisors attending Pioneer's retirement plan seminars call the idea "phenomenal" and "just what we've been waiting for." Clients have been clamoring for plans that will accept higher tax-advantaged contributions. Relatively higher costs have always been an issue. The "mini-K" answers both concerns.

Here is how key changes in the 401(k) rules (for those over 50) will benefit the one-person business starting next year:

1. Under current law, there is generally a 15% of aggregate compensation deduction cap on the combined sum that employers and employees can contribute annually to a 401(k) plan on a tax-favored basis. Next year the percentage amount increases to 25%.

2. The $170,000 compensation cap will increase to $200,000.

3. Unlike prior years, employee deferrals will not be counted toward the 25%-of-compensation limit. This will make it possible for a larger deductible employer contribution (up to 25%) plus the maximum $11,000 employee deferral in 2002 (up from $10,500 this year).

4. Individuals who are age 50 (or older) by the end of the tax year can make an additional "catch-up" contribution of $1,000 in 2002, to a 401(k) plan. (The law also allows for a $500 "catch-up" contribution to a SIMPLE plan.)

Additional advantages will accrue to those individuals who are also eligible to participate in an eligible 457 plan established by a tax-exempt organization or government employer because of the repeal of the coordination rules that previously limited elective deferrals to only $8,500.

There are several complications to the retirement plan calculations for the unincorporated business: the percentage-of-pay limits apply to compensation after plan contributions are subtracted and after deducting one-half of the self-employment tax. Therefore, that makes the 15% and 25% limitations more like 13% and 20% of earned income before the contributions. Note also that the combined employer and employee contributions are subject to a flat-dollar cap of $40,000 a person in 2002 (an increase from $35,000 this year).

Did Congress intend to hand out such a tax gift for the retirement plans of the one-person business? Probably not.

The tax law change that excluded 401(k) deferrals from the deduction-limit calculation was primarily intended to help low- and middle-income employees contribute more to their 401(k) plans, says Jim Morrell, a spokesman for Rep. Rob Portman (R-Ohio), who was one of the sponsors of the House tax bill.

But "even though Congress may not have intended to provide this benefit to a one-man plan, the law does," says Martin Nissenbaum, national director of retirement planning at Ernst & Ernst, New York.

The "mini-K" offers the largest potential benefit for one-person businesses earning between $50,000 and $170,000. The plan is not as compelling if the business is a sideline and the owner is also a corporate employee already participating in another 401(k) plan. An individual's combined deferral in both plans cannot exceed the $11,000-a-person limit in 2002 (plus catch-up contributions of up to $1,000 for 2002).

Costs and complexities of a "mini-K" must still be compared to those of Keogh, SEP, or SIMPLE plans--all of which were designed to be low-cost, uncomplicated plans for individuals and small businesses. While there are a number of lower cost 401(k)s available, set-up costs vary (up to as much as $3,000) with maintenance costs in addition. However, the Pioneer "Uni-K" plan is offered without any set-up charges plus annual charges of under $100.

In a business climate where the small business is a precarious business and tax laws often favor the large corporations, here's a break for the small business. Hooray for the little guy! *

The authors

William A. Clemmer and Gary S. Lesser, JD, head up Financial Services Agency Consulting (FSAC), a division of The Rough Notes Company. Clemmer has more than 25 years of financial services industry experience on Wall Street. Lesser writes and lectures widely on retirement planning and taxation issues. He is a member of the board of advisors for the Journal of Taxation of Employee Benefits.