Conning study explains underwriting superiority,

faster growth of regionals; agents not surprised

by regional company success

By Phil Zinkewicz

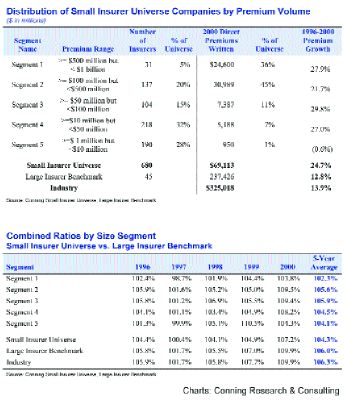

Conning found that between 1996 and 2000, small insurers increased their direct written premiums by 24.7%, nearly twice the 12.8% growth achieved by their large insurer counterparts. As a result, small insurers' market share grew from 19.4% in 1996 to 21.3% in 2000.

For the last decade, if not longer, property/casualty insurance industry observers, experts and analysts have been predicting the diminution--and possibly the demise--of small, regional insurers, at least of those smaller players in the marketplace. These predictions were not difficult to make considering the rapid changes that were taking place in the property/casualty insurance environment during that time frame.

First, there was the financial services convergence that dominated the marketplace in the late 1980s and early 1990s. Then, burgeoning technology demands were expected to overwhelm small insurance companies. Large insurers had massive capital resources and powerful economies of scale to extend their market domination over smaller insurers. Gramm-Leach-Bliley was expected to bring more competition into the property/casualty insurance marketplace--competition from non-insurance financial services entities, such as banks and securities firms. Larger insurers were expected to meet this new competition, but not small insurers.

Talk to insurance agents around the country, however, and you'll get a much different perspective. Independent agents call the smaller regionals the "backbone" of the insurance industry and say that they are faring much better than their counterparts in the "giant" insurance company sector. But, of course, that might be just talk. No one has done a study to determine how the smaller regionals have fared over the last, let's say, five years, right?

Think again. Conning Research & Consulting has taken on the task and recently released what is to be the first in a series of studies of the smaller insurance company market-place. And the first study shows that not only are small insurers surviving, but many seem to be thriving even amidst a rapidly changing insurance industry environment.

Jack Gohsler, senior vice president of Conning Research & Consulting, Inc., and co-author of a study titled Small Insurers - Thriving in the Land of the Giants, has this to say: "To understand why, you have to commit significant effort. There are many small insurers with many different strategies and operating models. Understanding these companies, even determining how many there are, is a daunting task. As a result, small insurers remain a nebulous, little understood and frequently ignored force in the property/casualty insurance marketplace."

To fill this information void, Conning is undertaking a series of studies to better understand small P-C insurers. Conning created a small insurer universe of 680 companies and established a large insurer benchmark of the 45 largest P-C insurers against which small insurers' performance can be measured. This first study focuses on underwriting--specifically premium growth and combined ratios.

Surprisingly, Conning found that between 1996 and 2000, small insurers increased their direct written premiums by 24.7%, nearly twice the 12.8% growth achieved by their large insurer counterparts. As a result, small insurers' market share grew from 19.4% in 1996 to 21.3% in 2000.

Conning also found that the small insurer universe achieved superior underwriting results. Small insurers achieved a five-year average combined ratio of 104.3%, while the large insurer benchmark group's combined ratio was 106.0%. In fact, says Conning, small insurers' combined ratios were lower than their large insurer counterparts in each of the five years included in the study. Conning says that these results appear to indicate that the benefit of market focus can overcome scale advantages.

Rough Notes obtained a copy of the full Conning study, which rigorously examines the small insurer universe, in an effort to understand why it has been successful. Growth and underwriting performance is examined by various size segments, a stock-mutual split, as well as geographical, consumer and line of business specialization. Conning also segmented the universe into eight company types to examine performance and facilitate further analysis of small insurers' strategies. And further analyses of small insurers will be forthcoming from Conning. In this article, we'll review the first of the series.

First, let's look at the study's methodology. Gohsler says that the small insurer study series is based on a detailed and statistical analysis of statutory data and interviews with industry leaders and managers within the small insurer universe. Conning also interviewed experts at the leading trade associations that serve or interact with small insurers, including: the National Association of Independent Insurers (NAII), the National Association of Mutual Insurance Companies (NAMIC), the Independent Insurance Agents & Brokers of America (IIABA) and the Professional Insurance Agents Association of America (PIA).

Gohsler says that Conning began its analysis from the base of companies filing annual statements with the National Association of Insurance Commissioners (NAIC). Within that base, there were 1,379 insurer groups and independent companies. Conning includes in the small insurer universe all companies with an average annual premium of less than $1 billion during the study period. Excluded from the universe were companies with less than $1 million in year 2000 premium volume; companies closely affiliated with another, larger property/casualty or life/health insurer; companies owned by large non-insurance U.S. or foreign parent; companies with separate statutory filings that were nevertheless closely related to other insurers in the universe; reinsurers; nontraditional insuring entities, such as state funds and limited ownership captives; and companies with insufficient data for inclusion in the analysis.

The exclusions resulted in a universe of 680 distinct insurers, according to Gohsler.

Conning found that most small insurers tend to focus geographically or by customer or product. "While a subsequent study will fully explore small insurers' strategies," says Gohsler, "Conning believes that a tight focus differentiates many small insurers, enabling them to grow faster and achieve better underwriting results than their larger insurer counterparts, because they know their market better, can respond to change more quickly and can also influence regulators."

Gohsler says that some industry experts had predicted that large insurers would use scale advantage to overwhelm their smaller competitors and that globalization and financial services convergence, along with technology challenges, were expected to marginalize small insurers.

"Conning's 2000 study, Property-Casualty Expense Management - Chipping at the Wrong Block in a Fragmenting Market, questioned that prevailing logic," says Gohsler, "finding that many of the larger merger and acquisition transactions had not been successful in reducing expense ratios. Research conducted in connection with that study concluded that, while the benefits targeted by these mergers proved elusive, integration proved especially difficult and associated costs often far exceeded plan."

Conning said there is growing evidence that focus may provide a competitive advantage, especially in lines of insurance that are primarily state-regulated. "A local focus enables insurers to know and serve their customers better and respond to marketplace changes more rapidly," says Gohsler. "Closeness to the market also may enable insurers to communicate with and influence regulators."

Conning also notes that, in both property/casualty and health/managed care, more companies are pointing to the benefits of focus.

To examine geographic reach more carefully, Conning divided its 680-company, small insurer universe into four groups based on premium distribution--single-state companies (287), single-state-dominated companies (107), regional companies (199) and multistate companies (96). All four groups grew at higher rates than the large insurer benchmark and achieved better five-year average underwriting ratios.

Line of business specialization is a key strategy for many small insurers. In fact, Conning classified 428 companies in its universe as line-of-business specialists. As a group, these companies grew roughly 2.5 times more than the larger insurer benchmark. "Line-of-business specialists grew at the highest rate of any of the specialist groups examined in the study," says Gohsler, "31.0%, far exceeding the growth achieved by the small insurer universe overall (24.7%) and the large insurer benchmark (12.8%)."

According to the study, line-of-business specialists also had the best underwriting results of any of the specialists groups--a five-year average combined ratio of 102.4%, vs. 104.3% for the small insurer universe overall and 106.0% or the large insurer benchmark.

The Conning study is an exhaustive one, delving into such market minutiae as: distribution of small insurer universe by premium volume, premium growth and market share by size segment, pure loss ratios by size segment, loss adjustment expense ratios by size segment, underwriting expense ratios by size segment, distribution of small insurer universe companies by corporate structure, insured loss ratios by geographic reach, premium growth and market share by customer specialization.

But the point is made, at least in this first of a series of studies on small insurance company markets. Small insurers have surprised--and appear to be positioned to continue to surprise--all the smart money that has bet on small insurance company extinction.

Those who are not surprised are independent agents. Jeff Peterson of the Pekin, Illinois-based Unland Cos., says his agency has always relied on smaller regionals because they have always performed well and he expects that they will continue to do so. "Regionals, in general, are niche players. They're focused. They don't try to be all things to all people the way the nationals do. They are close to the market and can make adjustments faster than the nationals can. Smaller regionals have their finger on the pulse of the insurance buyer."

Robert Loiselle of the Loiselle Agency in Pawtucket, Rhode Island, says that his agency is definitely growing more with regionals. "We have aligned ourselves with regionals because they are committed to independent agents as a distribution force and to the marketplace," he says. "In Rhode Island, regionals are increasing their market share, while the nationals are losing market share. You have to remember that Rhode Island is a fairly small market for a national. The entire market in Rhode Island is about a million and a quarter dollars. A national that might want to pull out of the market or diminish its presence, well that wouldn't even show up on the company's balance sheet. But that market is very important to regionals."

Loiselle pointed to one national insurer, Liberty Mutual, that has recognized the importance of the regional company market. "Liberty Mutual has a special division called regional agency markets. Even though Liberty Mutual is a direct market, about one-third of its business is generated in this division. Liberty writes the business but uses its stable of regional companies' brand names for its paper. That shows how important the market is to them."

Bruce Jacobson, of the Rhode Island-based Pearson Cronin and Jacobson, says that regionals are "bread and butter" to his agency. "Smaller regionals have a feel for what's going on in the marketplace," he says. "They have a much better handle on the local scene than do the nationals. And there is no comparison between the regionals and the nationals in terms of commitment to independent agents. Regionals are more committed to the agent because of their size. Because they are small, they need the independent agent."

Tommy Adams of Charles M. Moore in Bowling Green, Kentucky, says that his agency does about 98% of its business with regionals. "We find that they are more stable in terms of pricing and products," he says. "Regionals are able to react to changes in the marketplace much faster than nationals. They tend to get their underwriters out to the field more and build more personal relationships with agents and clients. And, let's not forget, this is a relationship business."

All the agents interviewed, then, agree wholeheartedly with the Conning study's findings. "Agents have been singing the praises of regional companies for years," says Peterson, "but nobody listens to us." *