Insurance agents could be the insurer of last resort

for toxic mold and environmental damages

By David J. Dybdahl, CPCU, ARM, MBA,

and Steven J. Lemon, JD

A rapid increase in fungus- and mold-related claims in the past two years has triggered new insurance exclusions that create new sources of demand for environmental insurance products and expertise. Innovative agents will be able to capitalize on this demand by offering appropriate coverage to their clients. These same agents will be able to completely avoid the downside of what is shaping up to be a professional liability problem for agents on an unprecedented scale.

In light of the magnitude of these loss exposures, it is surprising how complacent some insurance buyers, agents, and lenders have been in dealing with these newly uninsured loss exposures. One reason could be that it is very difficult for insurance consumers to put these new sources of uninsured loss exposures into perspective.

Although our historical loss data is still sketchy, what we think we know about mold claims is that, on average, they cost about as much as a fire loss, which is close to $20,000 per claim on a homeowners policy and $200,000 on a commercial property policy without a liability component (not that we want to downplay the liability component). In 2002 there were about 320,000 mold-related property insurance claims losses compared with 500,000 fire claims on commercial and personal lines policies. Like fires, mold can render an entire building valueless. As with fires, there are many mold-related remediation losses measured in the tens of millions of dollars. We know that fire losses cost insurers $12.6 billion in 2000. We believe that about $8 billion in mold-related damage claims were made under property polices in 2002. It is difficult to make an "apples to apples" comparison of these two sources of losses for the full 2002 calendar year because the new exclusions for mold-related losses seem to be working fairly well in deflecting most of the new mold-related losses back onto policyholders.

Toxic torts

Unlike fire losses, mold losses can give rise to an alarming phenomenon known as toxic torts. The loss costs mentioned above do not include losses from mold-related toxic torts. It is difficult to get a clear picture of how many liability claims are related to mold today because so few of them have actually been paid. Unlike fire insurance claims, toxic tort claims are the Energizer Bunny in the claims arena: They just keep going and going, looking for the ultimate deep pocket. Unfortunately, that ultimate deep pocket is most likely to be an insurance company. Sometimes a single toxic tort case on an apartment complex can reach $1 billion in alleged damages, although no plaintiff has ever been paid that amount.

It is difficult to explain some insurance buyers' complacency when exclusions for mold losses expose them to a greater degree of risk than does being uninsured for fire claims. In light of this exposure, it is also difficult to explain some agents' complacency when they are delivering these new exclusions. If agents were asked to deliver 50 million fire exclusions, their reaction would be different from their anemic response to the introduction of mold exclusions.

Historically, many agents also have ignored their clients' need for environmental insurance. Now, for the first time, these two sources of unnecessarily uninsured losses are being excluded in the agent's own professional liability policy. The confluence of these macro trends has--by fact, history, and circumstance--positioned agents to be the insurer of last resort for their clients' costly uninsured environmental and toxic mold claims.

In this article we will discuss the trends that led to this conclusion and present a simple loss prevention protocol that risk advisors can follow to avoid errors and omissions claims in this area, provide better service to their clients, and make a profit in doing so.

Damages from toxic mold have created unprecedented levels of professional errors and omissions loss exposure for agents. Toxic mold claims are much more frequent than either asbestos or environmental claims. Insurers have taken the lessons learned from their dismal experience with asbestos and environmental claims and moved in 2002 and 2003 to proactively exclude many mold claims from all property and liability policies. To completely shut the door on its exposure to uninsured environmental and toxic mold claims, even the professional liability market is adding new exclusions for mold and pollution "related" claims to agents E&O policies.

Insurance is available to cover environmental damages, including coverage for mold as a pollutant on commercial accounts and buybacks for mold damages from a small number of homeowners policies in many states. History shows, however, that the vast majority of agents will not advise their clients about the availability or importance of these coverages. As a result, insurance agents' professional liability underwriters this year have added fungus/mold and pollution "related" claims exclusions to avoid becoming the insurer of last resort on literally hundreds of thousands of newly uninsured fungus/mold and pollution claims. The new exclusions leave agents, not their E&O carriers, as the insurer of last resort for their clients' unintentionally uninsured environmental damages claims.

The new mold and environmental "related" damage exclusions in agents E&O policies are unusually onerous. Not only do they exclude claims for current activities, but they also exclude everything the advisor has done in the past that leads to an uninsured claim today. Agents E&O policies cover the claims made against them during the policy period for professional errors and omissions. Each new E&O policy purchased usually provides coverage for claims arising from new errors, acts, and omissions made during the policy period, plus all of the insured's prior acts. This means that the new mold and environmental "related" exclusions also will exclude everything the agent has ever done in the past to leave a client unprotected for environmental and mold losses.

Three waves of toxic mold claims

Three separate waves of claims will be generated by the toxic mold damages storm.

The first wave hit property insurers' beach in the form of claims for the remediation of mold-related damages, plus a heavy dose of bad faith claims adjusting by the insurance companies, and resulting bodily injury. When the first wave hit shore, the unsuspecting carriers writing homeowners insurance, especially in Texas, were swept off their feet. The mold claims were so severe for Farmers Insurance that it wanted to surrender its license and leave the state of Texas entirely. To regain their footing, in 2002 insurers began on a nationwide basis to add new exclusions for fungus/mold damages to all personal and commercial lines policies.

Foreseeing the transformation of property damage claims into liability claims, the insurance underwriting community actually built two breakwaters with its exclusions: one for property claims and one for general liability claims. The exclusionary breakwaters on homeowners, commercial property, and general liability policies will effectively shelter insurers from the oncoming waves. But these breakwaters will not protect insurers from claims for damages that occurred before the exclusions took effect on occurrence-based liability policies.

Trial lawyers are certain to become involved with the insured coverage disputes that will erupt as a result of the new fungus/mold exclusions. They are educated and ready to move in a coordinated fashion. Thousands of personal injury lawyers have already attended hundreds of seminars during the past four years where the words "Mold Is Gold" are used. These lawyers are unlikely to let recently minted exclusions on insurance policies prevent them from finding the ultimate party to pay for their clients' damages. In the absence of a single deep-pocket insurer, all they need to do is find a set of defendants whose combined assets make it worthwhile to pursue legal actions against them. These damage recovery efforts are certain to create two more waves of toxic mold claims.

The second wave of mold claims is approaching shore but has not yet crested. Tens of thousands of uninsured mold-related damage claims on commercial property and homeowners insurance policies will soon be transformed by plaintiffs' lawyers into liability claims for property damage and bodily injury. Although mold exclusions on property insurance may prove valuable as the breakwater for property underwriters, the property insurance breakwater may protect one beachhead at the peril of others. The newly excluded wave of property insurance claims will simply be deflected to property damage and bodily injury liability claims in other industries. Farther down the shore is the responsible party beach, an as yet unaffected shore inhabited by contractors, home builders, roofers, plumbers, engineers, building inspectors, architects, building products suppliers, real estate professionals, landlords, and similar classes of business who will be the targets of these deflected and now transformed property claims from the first wave.

Fresh from their experience in environmental damages from superfund and asbestos claims, the insurance companies wisely predicted the second wave of mold claims and built a second breakwater. They added mold exclusions to liability policies. Part of the energy from the second wave will be deflected back to sea by the general liability mold exclusion breakwater. That energy will not disappear, nor will the persistent plaintiffs' lawyers who will find the breakwater's resistance to be nothing more than a signal to look elsewhere for weaknesses. This can be seen as the impetus for the coming third wave.

Although exclusions for mold do nothing to protect the responsible parties, they do make them less attractive as individual targets for personal injury lawyers. In cases where enough defendants can be assembled to create an attractive asset base, however, an army of personal injury lawyers will pursue these damage claims on a contingency basis. The threshold damages amount to bring an action on a contingency basis could be as low as $30,000 in some venues. With the average mold remediation claim being in the $20,000 range, it will be easy to reach the dollar threshold by adding in attorney fees, additional living expenses, and medical monitoring.

With a long list of possible responsible parties for a mold damages case, assembling an attractive asset base, even if there is no insurance, will be relatively simple for personal injury lawyers. The second wave of mold damage claims will create uninsured liabilities for thousands of defendants. In the discovery process the record will show that many of these firms could have purchased environmental insurance covering mold-related damages and this will be the beginning of the third wave.

The third wave of professional liability claims against risk advisors now is just a swell off shore, barely noticeable to the casual observer. This wave is headed directly for the risk advisors who left their clients unintentionally uninsured against the mold damage storm. Broader in its base than the first two waves, the third wave will pick up the energy that was deflected by the first two breakwaters.

The risk advisor professional liability beachhead sits between the two breakwaters constructed by insurers for property and liability claims, totally unprotected from the storm. As the third wave approaches shore, the breakwaters constructed by insurers will channel it to give it more height. The initial energy of this wave (uninsured toxic mold property and liability claims) will be amplified by legal expenses, as well as personal injury and bad faith claims. As this swell intensifies, observers will see that it consists entirely of uninsured claims seeking to come as far ashore as possible in hopes of unleashing a great fury on some "liable" parties.

Few safe harbors will protect risk advisors from the third wave. This wave threatens to wash over risk advisors who have little or no defense, making landfall as professional liability claims against them. Agents and brokers, as well as risk management consultants and lawyers, all of whom advise their clients on issues of risk management and insurance, will be caught in this maelstrom for failing to advise, recommend, and/or procure for their clients the appropriate insurance against environmental and mold-related losses.

Five-step protocol

Agents can avoid potentially uninsured E&O claims by following a simple five-step protocol that is designed to provide a high degree of professional service to the client and eliminate E&O claims arising from a client's unintentionally uninsured environmental and mold losses. By implementing today the five-step process outlined below, agents also can erase professional liability loss exposures from the past.

1. Establish the scope of work to be undertaken on behalf of each client.

2. Advise clients about their exposure to loss by determining the environmental risks each client faces.

3. Advise clients about insurance that is available and how the environmental exclusions in certain policies can leave them uninsured for particular losses.

4. Recommend the purchase of and, if appropriate, offer to procure for clients the appropriate insurance, as it becomes available in the market place.

5. Complete the work by providing clients with written statements that document the agent's activities and the client's responses.

Risk advisors as the insurers of their clients' negligence

Risk advisors who have not implemented the five-step environmental risk management protocol could even become the insurer of last resort for the negligence of their clients. For example, construction defects that allow water intrusion in buildings often result in mold damage claims. These mold damage claims against the contractor could easily be transformed through the negligence of the insurance intermediary into a professional liability claim against the intermediary for leaving its client uninsured. Environmental impairment liability insurance to cover the mold-related damages of contractors has been available in the insurance market place since 2001, with minimum premiums as low as $2,500. The professional standard of care required for insurance intermediaries in the state the contractor is domiciled in, and how well the agent or broker implemented its five-step environmental loss control protocol will determine the degree to which the agent or broker will be responsible for the uninsured general liability claim of its client.

Risk advisors are relatively easy targets

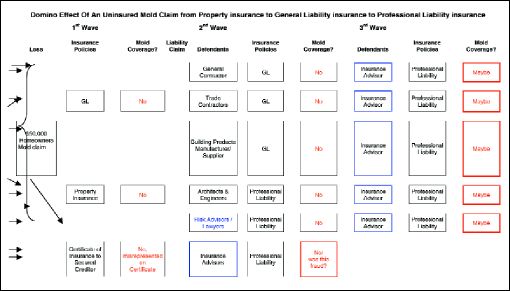

As armies of well educated and coordinated plaintiffs' lawyers bear down to recover damages and legal fees on tens of thousands of mold-related damages cases, universal mold exclusions and limitations in new and renewal insurance policies will create a domino effect of successive claims into new classes of defendants--ultimately a third wave of professional errors and omission claims being made against risk advisors for failure to procure the appropriate insurance for their uninsured clients. This sequence is shown in the chart on page xx titled "The Domino Effect of an Uninsured Mold Claim."

Agents and brokers rarely use the five-step process to address their clients' environmental loss exposures. Most assume step 1 is understood and usually just point out the new mold exclusion without addressing steps 2, 3 and 4, which leaves the door wide open in most states for an E&O claim if a client has an unintentionally uninsured loss. Perhaps even more troublesome is the fact that step 5 often is not even considered by persons whose main responsibility is to manage losses through the appropriate use of written contracts.

As a precaution against the third wave of mold damage claims, agents should be sure to follow three guidelines when preparing the completion statements noted in step 5. First, the completion statements must comport with the applicable established scope of work. Second, the completion statements must advise the client that the extent and value of coverages will change over time and with changes in the business. Third, the completion statements must advise the client that the agent's work is completed and that the client has requested no further work

Agents' legal responsibilities for complying with professional standards vary from state to state. Regardless of the legal responsibilities, implementing the five-step protocol makes sense from the business relationship standpoint alone. No agent wants to break the news to a client that there has been a surprise uninsured loss, and no agent wants to stand unprotected against the third wave of mold damage claims. *

About the authors

David Dybdahl is an environmental specialty wholesaler and senior consultant with American Risk Management Resources Network, LLC, in Middleton, Wisconsin, specializing in environmental risk management and insurance. He can be reached at dybdahl@armr.net. Steven Lemon is an attorney specializing in environmental law in the firm of Jones Lemon Graham & Clancy in Geneva, Illinois. He was an editor of the Harvard Environmental Law Review at Harvard Law School. He can be reached at StevenL@JonesLemon.com.

Excerpts from this paper have been previously published in the Winter Edition of the Environmental Claims Journal Winter 2003. Permission to use this material was provided by Taylor & Francis. The Society of Property and Casualty Underwriters has also published excerpts from this paper in its summer and fall editions of Insurance Agent & Broker and Underwriting interest section newsletters. Permission to use this material was provided by the American Institute of CPCU.