|

|

|

|

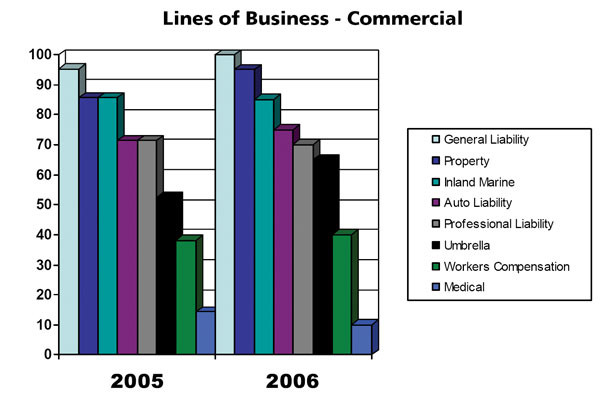

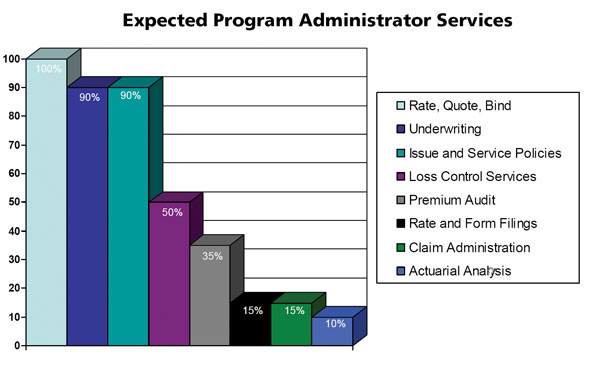

Survey highlights trends in program administration Guy Carpenter reports on insurer preferences in working with program administrators By Phil Zinkewicz “The nature of risk is increasingly complex and constantly changing. Some risk management challenges are obvious. Others less so, mostly due to events beyond your control or that have yet to be contemplated. Add the scrutiny of regulators, ratings agencies and other stakeholders, and the hurdles are even higher. With your capital at stake, you need a risk and reinsurance advisor with a track record of visionary ideas and delivering on its promises.” That quotation is from the Web site of Guy Carpenter & Co., Inc., one of the world’s foremost reinsurance intermediaries and a subsidiary of Marsh & McLennan, the largest insurance broker of the world. The statement is self-promotional, of course, as most Web site introductory statements are expected to be. It is followed by a description of the professionals in the reinsurance industry who are part of the Guy Carpenter team, and the wealth of knowledge and experience that the company has amassed over the years. Those in the front lines of the insurance business—the agents and brokers, the managing general agents, the program administrators—might look at Guy Carpenter as an organization far removed from the day-to-day operations of the primary insurance market. But today’s reinsurance environment is not the old boy’s exclusive club of 30 years ago. We have come to a point at which reinsurers and their brokers and intermediaries are very interested in what is happening in the trenches. A recent survey by Guy Carpenter is an example. The reinsurance intermediary’s Program Manager Solutions Specialty Practice has surveyed, for the second consecutive year, a number of domestic insurance companies that entertain specialty programs written through program administrators. Carl Bach, senior vice president and head of the Practice, says that the survey’s goal is to “illuminate” these companies’ appetites and requirements for program business. “Our treaty clients, which are insurance companies, number somewhere north of 1,000,” says Bach. “We have an equal number of prospective clients. Many of them are involved in program business. We wanted to provide MGAs and program administrators with the information they need to satisfy our clients’ appetites and, at the same time, provide our clients with the opportunity to explore programs they might not see on their own.” Bach says that the survey results provide an overview of issuing carriers, their program appetites, program administration criteria, claims administration requirements, monitor and control practices, reinsurance purchasing practices and views of specialty program market conditions. The survey was conducted via e-mail to key individuals at insurance companies that write a significant amount of program business through program administrators, he says. “Over the years, the specialty program market has grown to include both traditional insurance companies with a specialty program division and companies whose business model is to write specialty programs exclusively,” says Bach. “The majority of this year’s survey respondents (65%) describe themselves as writing specialty programs exclusively, up from less than half (48%) of respondents last year. However, regardless of whether their business focuses exclusively on specialty programs, the survey suggests that carriers have the ability to write programs in most of the 50 United States and utilize either admitted or nonadmitted paper, or both.” Bach says that the survey shows that companies appear to be “migrating” toward nonadmitted paper. “Last year, some 90% of respondents were licensed in 40 or more states for admitted and/or nonadmitted paper,” he says. “This year, the percentage of respondents saying they were licensed to write on nonadmitted paper in 40 or more states jumped to 94.1%, while a lower 78.9% of respondents report being licensed to write on admitted paper in 40 or more states.” Bach says this move towards nonadmitted paper is the result of more flexibility of rates and forms and the ability to control costs. The aggregate premium writings of responding carriers were just over $6 billion at year-end 2005, according to the survey, underscoring their commitment to the program market segment. Responding carriers projected that they will write a total of at least 80 to 100 new programs in 2006 and expect their resulting premium volume to exceed $7 billion. As far as lines of business, (See Lines of Business Graph on page 46.) the survey shows that responding carriers can write most commercial lines of business in today’s marketplace. A full 100% of respondents noted an appetite for general liability insurance. The majority also indicated an appetite for property, inland marine, automobile liability, professional liability and umbrella liability. Fewer indicated writing workers compensation (40%) and medical (10%). The most significant change from last year, according to Bach, is evidenced in commercial umbrellas, with some 65% expressing a willingness to underwrite that line now as compared to 52% last year. “With respect to personal lines (homeowners, auto and umbrella), it appears that more companies are looking to grow their personal lines programs,” says the survey. “This year, 65% of the respondents indicated a desire to write personal lines as compared to only 42% last year, with 30% having interest in homeowners, 25% indicating an appetite for auto, and 10% for umbrella.” The survey shows that responding carriers seem to vastly prefer programs that are regional (65%) over national (25%) and single-state (10%) programs. “This is a dramatic shift from 2005 when respondents were fairly evenly split, with 40% saying they preferred regional programs and 30% each indicating a preference for either national or single-state programs,” says Bach. He also said the shift to regional programs could be related to climactic changes that have taken place in some parts of the country in the last couple of years. Moreover, Bach says, this year’s survey reveals movement toward a lower targeted annual program premium size compared with 2005. Forty-five percent of responding carriers indicate they are looking for $10 million to $15 million in annual gross written premium, compared with 50% a year ago. Thirty-five percent indicated a preference for smaller programs (below $10 million), up from 25% last year. Only 20% of respondents indicated a preference for larger programs (above $15 million), down from 25% in 2005. The survey also shows that respondent carriers expect their program administrator to rate, quote and bind business in their behalf. (See Expected Program Administrator Services Graph.) A full 90% of respondents expect or allow the program administrator to perform the underwriting function as well as issue and service policies. “This marks an increase over last year when 81% of respondents indicated a desire for underwriting and just over 75% indicated a desire for issuing and servicing policies,” says Bach. “More than half of respondents (55%) expect loss control services from their program administrator, while 35% allow for the outsourcing of the premium audit. Only 15% expect rate and form filings as well as claims administration, and 10% expect actuarial services to be performed by their program administrator partners.” Says Bach: “Given the significant number of responding carriers that allow the program administrator to perform underwriting and policy issuance services on their behalf, one can understand why carriers require program administrator partners to carry adequate E&O and fidelity limits, although the limits required vary,” said Bach. Bach describes the variances found in the survey: • Thirty percent of respondents this year say that they require at least $3 million to $5 million in E&O limits. The number mandating a minimum of $1 million to $3 million in E&O limits dropped to 30% in this year’s survey compared with 50% a year ago. Only 15% of respondents this year require $5 million to $10 million in E&O limits, down from 28% a year ago. • Some 55% of respondents require more than $1 million in fidelity limits, while 25% require limits greater than $5 million. • In exchange for requiring program administrators to take on a variety of traditional insurance company services, a full 90% of responding carriers appear willing to pay commission levels commensurate with the services provided, rather than a predetermined percentage in excess of commissions paid to their production sources. • In line with the desire of carriers (and their reinsurance partners) to increasingly align the interest of all underwriting parties, a number of responding markets are requiring a level of risk sharing on behalf of the program administrator. • Approximately 65% of respondents appear to believe that a sliding scale commission is an appropriate alignment, up from one-third last year. Nearly half (45%) of responding carriers are still paying flat commissions. In those instances where risk sharing is required, greater than half (55%) of respondents report utilizing a number of other available or allowed vehicles, including an agency captive, a carrier’s rent-a-captive facility, a third-party rent-a-captive facility or a group/association captive. The survey goes on to address such subjects as claims handling, the use of third-party administrators, monitoring and, not unexpectedly, reinsurance issues. “The reinsurer is an important specialty program partner,” says Bach. “A carrier supporting special programs can either roll a program into its corporate treaties or elect to purchase program-specific reinsurance. Sixty percent of carriers responding to this year’s survey indicate a preference for rolling a program into the corporate treaties, as compared to 48% last year.” Copies of the full survey results are available for download at www.guycarp.com. For printed copies, contact Guy Carpenter at marketing@guycarp.com. * |

|

|||||||||||||

| ||||||||||||||