|

|

|

|

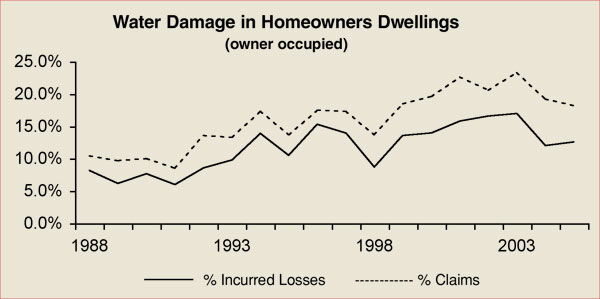

AAIS Perspective Avoiding leaks Revised AAIS homeowners forms refine provisions in response to growth in water losses By Joseph S. Harrington, CPCU Has the rising tide of water damage claims in homeowners insurance crested?Maybe so, according to data from the American Association of Insurance Services (AAIS), but it’s too early to tell whether the tide has turned for good. AAIS is a national advisory organization and licensed statistical agent based in Wheaton, Illinois, that develops policy forms, manual rules, rating information, and statistical plans used by more than 600 property/casualty companies throughout the United States. For purposes of statistical reporting, the term “water damage” refers to property damage caused by a sudden, accidental, and unexpected discharge of water within a structure, such as when a washing machine breaks and dumps water onto floors and carpeting. In recent years, however, mold losses added a new dimension—and increased losses—to the concept of insured water damage. Also, from a statistical reporting perspective, insured water damage does not include damage caused by flood or surface waters, which has been explicitly excluded from coverage, or damage from wind-driven rain, which is reported under wind and hail coverage. Statistics According to AAIS statistical data for homeowners insurance, losses reported under “water damage” doubled over the course of a decade as a percentage of total losses reported for owner-occupied homes. On average, water damage accounted for 11% of homeowners claims per year for the period 1988-93, but rose to 21% of claims for the period 1998-2003. For the same periods, water damage rose from an annual average of 7.7% of annual incurred homeowners losses in 1988-93 to 15.4% in 1998-2003. Similar results emerge from other industry data. The Insurance Information Network of California (IINC) reported in 2002 that “the cost of water damage [in California] has climbed in each of the past four years.” An IINC survey of insurers found that water-related claims accounted for nearly one-third of California homeowners claims in 2001, and that the average severity of a water damage claim nearly doubled between 1997 and 2001, from $2,537 to $4,730. In a 2003 report on mold, the Insurance Information Institute (I.I.I.) stated that “in only two years, claims costs have skyrocketed. “The typical homeowners mold claim now costs $15,000 to $30,000 to handle, compared with $3,000 to $4,000 for the average homeowners claim not involving mold,” the I.I.I. report added. Turning point? AAIS loss data indicate that homeowners water damage claims and losses have fallen off since hitting their peak in 2003. Water damage accounted for 23.3% of claims for owner-occupied homes reported to AAIS for 2003, before falling to 19.2% of claims in 2004 and 18.2% in 2005. Similarly, losses from water damage fell from a peak of 17% of incurred losses in 2003 to 12% of incurred losses in 2004 and remained essentially level at 12.6% in 2005. The table on page 98 shows this is not the first time water damage claims and losses have declined, but there are several reasons why the latest downturn could reverse the upward trend. For one thing, companies have embraced underwriting discipline in homeowners to a degree hardly imagined in the 1990s. Part of that underwriting discipline entails systematic use of loss history databases, such as the Compre-hensive Loss Underwriting Exchange (CLUE), to identify individuals and properties that are the source of water-related claims. This effort has caught the attention of the national media, which have produced numerous reports cautioning consumers that they risk being rejected, cancelled, or non-renewed for homeowners insurance if they submit too many claims, particularly for water damage that can be prevented or corrected through regular maintenance or cleanup. Second, most insurers have implemented coverage exclusions and limitations for losses arising from mold and other fungi. These were developed by AAIS and other organizations in the wake of the surge in mold claims in 2001, and implemented countrywide following their approval by regulators. Also, the insurance industry has engaged in a public relations effort to call attention to the rising volume of water damage claims. As we’ve seen, organizations like IINC and I.I.I. issued reports on the growth of water-related losses and the threat they posed to homeowners insurance affordability. In addition, the Institute for Business and Home Safety, an insurance industry-sponsored organization created to help mitigate losses from natural disasters, has gone beyond its original mission to mount a campaign addressing costly but not disastrous water damage to structures. Refinements Whether the latest drop in water losses proves to be temporary or long lasting, AAIS has refined water-related provisions in its newly revised homeowners forms, now being field tested countrywide and scheduled to start taking effect in 2007. The purpose of those refinements is to preserve the basic intent of homeowners policies, which is to provide protection against fortuitous loss, not funding for home maintenance. In one example, an open perils exclusion previously named “Seepage and Leakage” has been renamed “Water, Humidity, Moisture, or Vapor” to reflect changes in its scope. The new exclusion specifies that it applies to losses arising from continuous or repeated seepage, leakage, or discharge of water, or from the presence or condensation of humidity, moisture, or vapor. The exclusion adds that it applies to such losses when they occur over weeks, months, or years, thus clarifying that the exclusion is not intended to apply to sudden and accidental events. Also, the exclusion does not apply to losses as described above, even those that occur over prolonged periods, if the insured could not reasonably be expected to suspect the damage was occurring. Complementary changes have been made to the insured peril called “Accidental Discharge or Overflow of Water or Steam.” Using language identical to that in the “Water …” exclusion discussed above, the accidental discharge peril states that it does not apply to continuous or repeated discharge, seepage, or leakage. It, too, grants an exception (preserving coverage) for losses over a prolonged period that no insured would reasonably suspect. In addition, the revised AAIS homeowners forms feature a built-in exclusion for “Bacteria, Fungi, Wet Rot, or Dry Rot.” This exclusion incorporates provisions from recent “mold” endorsements with a long-standing exclusion for mold, wet rot and dry rot, which were previously addressed in “wear and tear” exclusions. As its title suggests, the “Bacteria, Fungi …” exclusion has been expanded to encompass bacteria and all fungi, not just mold, and it also excludes cost or expense caused by those organic substances. However, the exclusion makes exceptions preserving coverage for bacteria, fungi, etc., that result from an insured peril, as well as for losses caused by an insured peril, such as fire, that results from the presence of bacteria, fungi, etc. Careful attention to policy provisions, combined with sound underwriting, can help insurers maintain water losses at a stable level and preserve the nature of homeowners coverage as it was originally envisioned. * This article is general in nature and is not intended to provide definitive information regarding use of AAIS products and services, which is restricted by copyright and license agreements. This article in no way alters, supplants, or supersedes what is written in AAIS policy forms, manuals, bulletins, or other communications, and does not indicate any official AAIS position on the matters discussed in the article. The author |

|

|||||||||||||

| ||||||||||||||