|

|

|

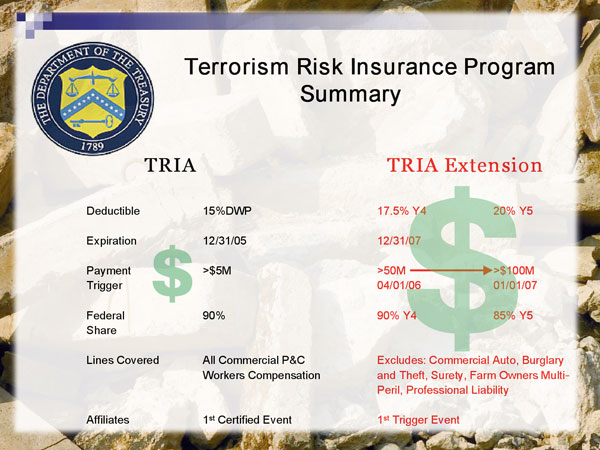

Life without TRIA The industry does not have the resources to go it alone By Michael J. Moody, MBA, ARM The terrorist attacks of September 11, 2001, caused ripple effects throughout the U.S. economy. One of the biggest ripples was within the insurance industry. Due in large part to the scope of the losses following the attacks, some concern existed regarding the industry’s ability to pay its losses. Over time, however, that has resolved itself as claims were settled and the industry stepped forward to respond to its policyholders in a timely fashion. While the events of that day did have an impact on most insurers’ financials, they moved onward; but despite this, a concern about future terrorist events quickly grew. Prior to 9/11, terrorism coverage was a minor issue. Coverage for the most part was automatically included within most commercial insurance policies. However, after 9/11, the treatment of terrorism coverage has been anything but a minor issue. The Terrorism Risk Insurance Act (TRIA) Shortly after the 9/11 events, insurers began to eliminate or greatly reduce their coverage for terrorism. It quickly became clear that the limited availability of coverage for terrorism, particularly in high-risk areas, would have a profound impact on the U.S. economy. As a result, Congress passed the Terrorism Risk Insurance Act (TRIA). The Act was signed into law by President Bush on November 26, 2002. One of the main features of the Act was that, in the event of another terrorist attack, it would allow the insurance industry and the federal government to share the resulting losses in accordance to a specific formula. While there were precedents for such a private/public partnership, TRIA was noteworthy since it enabled the insurance market to begin rewriting terrorism coverage immediately since the federal backstop of TRIA would effectively limit insurers’ losses. The Act provided a methodology where the insurance industry could continue to provide terrorism coverage in the short term, while they worked on a longer term solution. This was an important aspect of the legislation—it was only intended as a temporary solution. To assure that another solution was developed, TRIA contained a sunset feature that was effective on 12/31/05. From all respects, it appears that TRIA was successful in fulfilling its original goal of resolving the affordability and availability issues that surrounded terrorism coverage subsequent to 2001. Coverage for terrorist acts was once again available in the general insurance markets. And a number of different industry segments were quick to accept the new coverage options. Among the groups actively seeking coverage were financial institutions, real estate firms, and health care facilities. Coverage was also popular in high-risk, downtown city locations. Brokers were reporting up to 60% to 70% of these high-risk locations were taking terrorism coverage. Alternative market involvement As marketplace displacement became common, captive insurance companies have stepped in to fill the needs of their parents. From the start, it was determined that U.S. domiciled captives would be considered as “insurers” for the purpose of TRIA. This basically meant that U.S. captives were entitled to all of the TRIA benefits and subject to all the requirements. Non-U.S. based captives, however, were not subject to the TRIA legislation. In the past, captives have frequently been used as viable alternatives to solve insurance marketplace affordability and availability issues, and terrorism coverage was no different. In fact, with TRIA, there were major advantages to include terrorism coverage within the captive. Among the numerous advantages that captives could provide to their owners, as compared to the traditional insurance market, are broader coverage, which can be tailored to the parent’s needs; possible return of premiums if no losses occur; and the ability to cover exposures that the commercial market has trouble covering. This would be especially true for terrorism coverages involving nuclear, biological, chemical and radiological exposures that are usually excluded from traditional terrorism coverage. The primary benefit of the TRIA backstop for all insurers, including captives, has been the substantial amount of protection the TRIA program provides, up to 90% of the policy limits. Typical requirements that are noted in regards to TRIA and that are applicable to captives include making coverage available for only “certified acts” of terrorism and satisfying certain disclosure and reporting requirements. Overall, however, existing captives have found a number of advantages to extending terrorism coverage to their parents. One of the issues that a captive had to deal with when adding terrorism coverage was the approval of its domiciliary regulator. Approval for existing captives was typically quite easy once regulators had assured themselves that the plan of operation was prudent. Among the things that would be taken into consideration were premiums to be charged, capitalization of the captive and the financial strength of the parents. Regulators, and for that matter, the Treasury Department, have noted the value of the captive industry in resolving this terrorism coverage issue. TRIA extension The sunset feature of the original TRIA legislation was due to expire on December 31, 2005. Without going into great detail about the pros and cons of the extension, on December 22, 2005, Congress did in fact decide to extend the Act for two more years. However, they did modify the original Act in several important ways. Among the key features were the following: • Increased insurer deductible to 17.5% of prior year’s direct earned premiums in 2006 and 20% in 2007. • Aggregate industry retention levels increased to $25 billion in 2006 and $27.5 billion in 2007. • Annual aggregate cap on loss payments of $100 billion for both 2006 and 2007 program years. • Insurer deductible comprises a 10% coinsurance in 2006 and increases to 15% in 2007. However, the most important feature to be changed is the loss trigger aspect. While the loss trigger of $5 million remains, a new condition provides that no federal payments will be made to any insurance companies unless the aggregate-per-occurrence-industry-insured losses exceed $50 million in insured losses in 2006 and $100 million in 2007. It’s this final change, the loss trigger, that has required most captives to review their participation in the terrorism coverage market. As a result of this new loss trigger, it is possible that those captives that have TRIA deductibles of less than $50 million will reconsider participating in the primary layers of coverage. It is especially true if additional capitalization or additional reinsurance would be required to make up the $50 million exposure. This whole issue could well end up with further evaluation of capital adequacy for the “trigger” exposures noted above by the captive domicile regulator. Ultimately the captive may decide to abandon its involvement with terrorism coverage altogether and the parent could merely opt to go uninsured. TRIA’s end game By adding terrorism coverage, captives have for the past few years, found yet another value-added service that they can provide to their parents. However, with the advent of the TRIA extension, this may have been diminished somewhat. Of course the bigger question is what will happen when the extension expires at the end of 2007. This is really the key issue involved with the current terrorism coverage option. From the start, TRIA was promoted as a temporary solution, to give the industry a chance to find a permanent solution to the terrorism coverage issue. In part, the extension was allowed due to the significant losses suffered by the industry from Hurricanes Katrina, Rita and Wilma; however, the question remains: What will happen at the end of 2007? Numerous reports from interested groups and associations have been noted recently. Unfortunately, most of the plans that have been advanced have totally ignored the obvious desire of the federal government to abandon its role in this situation. At this point, many experts agree that the insurance industry simply does not have the financial resources to survive another terrorist attack. Given this reality, perhaps it’s time to take advantage of the various capital market alternatives and look to the alternative risk transfer market for a permanent solution. * |

|

|||||||||||||||||

| ||||||||||||||||||